Barclays is enabling customers to block certain categories of spending to help them take control of their finances.

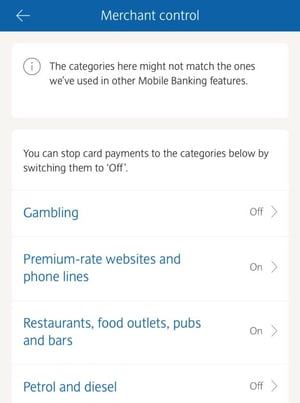

Following research, it identified five categories of retailers which customers wanted help in managing:

- Groceries and supermarkets

- Restaurants, takeaways, pubs and bars

- Petrol and diesel

- Gambling, including gambling websites and betting shops

- Premium rate websites and phone lines, including TV voting, competitions and adult services

Customers can now ‘switch off' these types of retailers through the Barclays mobile app by the click of a button - or over the phone or by going into a branch.

If customers try to make a payment to a retailer they've switched off, it will be declined automatically.

If customers try to make a payment to a retailer they've switched off, it will be declined automatically.

It’s looking to apply the same tool to credit cards at a later date.

Will it actually help?

According to Martin Lewis, founder of MoneySavingExpert and the Money and Mental Health Policy Institute, yes.

“Many have asked 'surely people can just gamble in cash'? Yes they can, and there are other work arounds too. However our Money and Mental Health Policy Institute research shows the key to all of this is friction.

“Making something more difficult to do, slows people down, and gives time to consider. This is important when you're dealing with impulse control.

“It has long been used in other sectors, e.g. blocking pharmacies selling people more than 32 paracetamols, makes it more difficult for someone to buy enough to overdose. Of course people can go to more than one store, but the conscious act of having to do that because people are trying to prevent it, is a barrier.

“With blocking gambling transactions (or premium phone lines as Barclays also allows) on a card, the fact you chose to do it, adds an emotional significance to working around it - i.e. you've committed to not gambling, and now you're changing.

“So friction is just as much a behavioural blocker as a transactional one. It isn't perfect. It won't stop everything, yet hopefully it is another tool to help people control themselves. And my hope is others banks will follow suit.”

A first in banking?

Not quite.

Whilst it’s the first of the High Street banks to do this, digital banks Monzo and Starling – the agile players, unconstrained by legacy technology - already offer this to customers.

Monzo launched its tool in June, which actually goes a little further and requires 48 hours' notice from customers to lift the restrictions.

It’s reported a 70% decline in spending on gambling as a result.

The challenger bank has made further innovations to support vulnerable customers. Earlier this year, it developed a tool that lets customers tell them about their circumstances from the Help tab in their Monzo app.

Growing need for change

There has been mounting pressure for financial services organisations to better serve vulnerable customers.

Last year’s Financial Lives survey by the Financial Conduct Authority (FCA), found that 50% of UK consumers show one or more characteristics of potential vulnerability.

------

Read our vulnerable customer interviews with Jake Mills from Chasing the Stigma, Mark McElvanney from StepChange Debt charity, and Liz Bates, former CEO of Deafblind UK.

Interested in talking to one of our consultants?